Jobs report drops mortgage rates

By Palm Beach Business.com

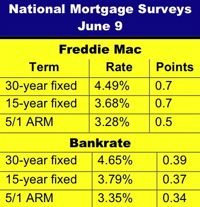

DELRAY BEACH — Mortgage rates continued fall over the past week, hitting new lows for the year in the Freddie Mac survey and dropping for a ninth consecutive week in Bankrate’s.

DELRAY BEACH — Mortgage rates continued fall over the past week, hitting new lows for the year in the Freddie Mac survey and dropping for a ninth consecutive week in Bankrate’s.

Last week’s job report from the Labor Department, the subject of much hand wringing among investors and analysts, served as the latest catalyst.

Freddie Mac’s Primary Mortgage Market Survey found the average 30-year fixed-rate mortgage dropping to 4.49 percent with 0.7 point, down from 4.55 percent a week ago.

Bankrate’s national mortgage survey put the 30-year at 4.65 percent with 0.39 point, down from 4.69 percent a week ago.

"Long-term Treasury yields moved lower following a weak jobs report and mortgage rates followed suit,” Freddie Mac Chief Economist Frank Nothaft said. “The economy added 54,000 jobs in May, the fewest in eight months, and factories cut payrolls for the first time in seven months. As a result, the unemployment rate rose to 9.1 percent, representing the highest rate since December.”

Mortgage rates typically move with Treasury yields, particularly the 10-year bond.

Bankrate noted that the jobs report was just the latest in a string of weak economic results that have brought yields on ten-year Treasury notes below 3 percent, and pulled mortgage rates lower for nine consecutive weeks. Fixed mortgage rates are at the lowest levels since last Thanksgiving and most adjustable rate mortgages have established new record lows.

The 15-year fixed-rate mortgage dropped to an average of 3.79 percent with 0.37 point in the Bankrate survey, down from 3.88 percent a week earlier. Freddie Mac put the 15-year at 3.68 percent with 0.7 point, down from 3.74 percent a week earlier.